Electronic Records and Digital Evidence under New Act

Tax administration has decisively moved into the digital era. Under the New Income-tax Act, electronic records and digital evidence are no longer supplementary. They are now central to assessments, reassessments, surveys, searches, and appellate proceedings.

Understanding how digital evidence is recognised, evaluated, and challenged has become essential for every taxpayer and tax professional.

Meaning of Electronic Records and Digital Evidence

Electronic records include any information generated, received, stored, or transmitted in electronic form.

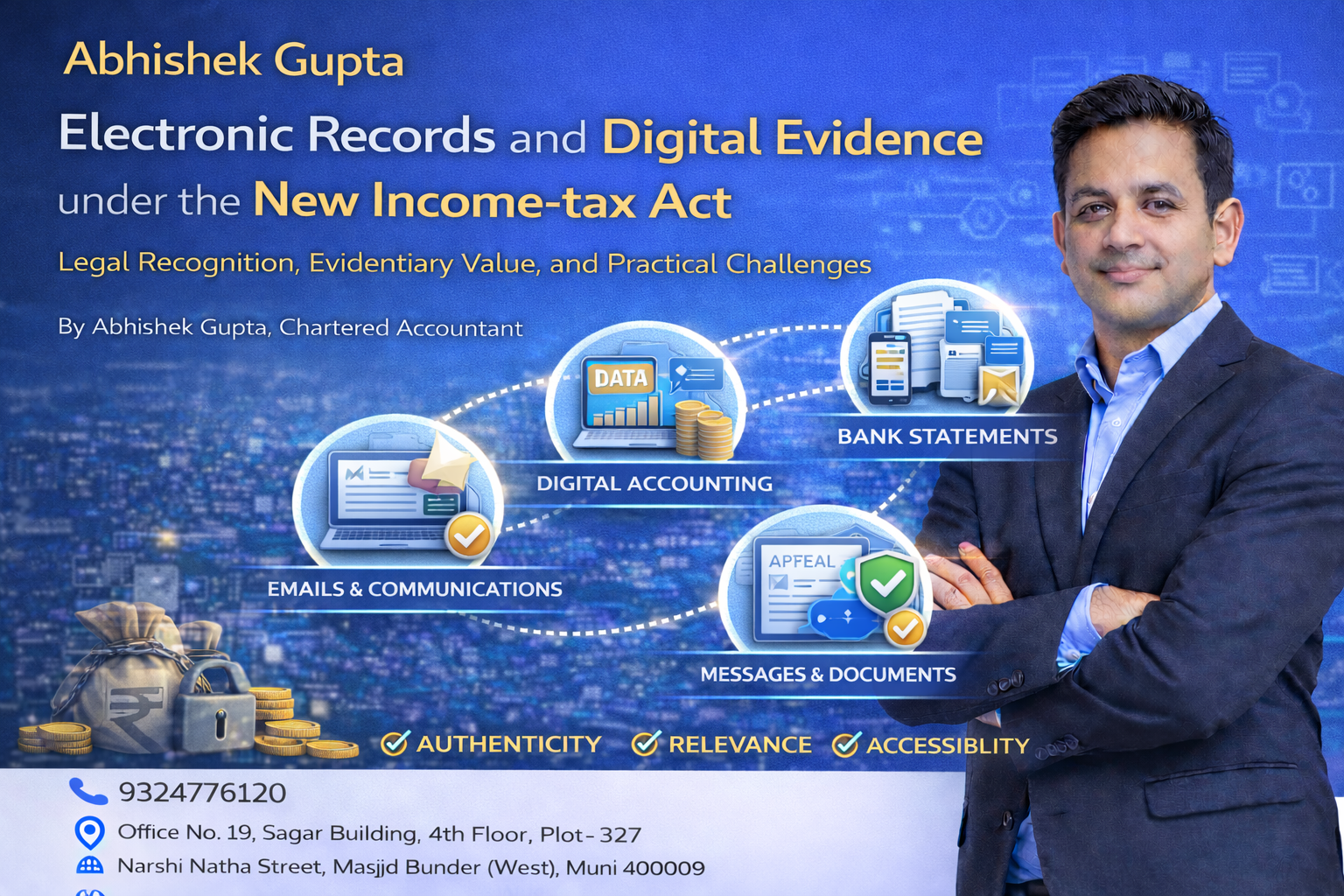

This covers:

Emails and electronic communications

Digital accounting records

Bank statements and transaction logs

Cloud-stored documents

WhatsApp messages and SMS (where relevant)

System-generated reports and analytics

Under the New Act, such records have explicit legal recognition.

Legal Recognition under the New Framework

The New Income-tax Act aligns tax proceedings with modern evidentiary standards.

Electronic records:

Are admissible as evidence

Can form the basis of additions and disallowances

Are routinely relied upon in faceless assessments

However, admissibility does not automatically mean conclusive proof.

Evidentiary Value of Digital Evidence

Digital evidence must satisfy:

Authenticity

Integrity

Relevance

Proper linkage with the taxpayer

Courts have consistently held that:

Raw digital data without verification has limited value

Electronic records must be corroborated with surrounding facts

Context matters more than isolated extracts

Data without explanation is not evidence.

Evidence requires interpretation.

Use of Digital Evidence in Assessment Proceedings

Assessing Officers increasingly rely on:

AIS and TIS data

Bank transaction analytics

Digital trails from GST and financial platforms

Electronic confirmations and statements

While such data strengthens detection, mechanical reliance without verification violates natural justice.

Taxpayers must be given:

Opportunity to explain

Access to relied-upon material

Time to rebut digital findings

Electronic Evidence in Search and Survey

During search and survey proceedings, authorities may:

Access digital storage devices

Copy electronic records

Examine cloud-based data

However:

Unrelated personal data cannot be used indiscriminately

Digital evidence must relate to undisclosed income

Additions must be based on incriminating material, not volume of data

Digital fishing expeditions do not survive appellate scrutiny.

Challenges and Risks for Taxpayers

Common risks arising from digital evidence include:

Misinterpretation of emails or chats

Incomplete data extraction

Out-of-context reliance on messages

Automated mismatch flags without human review

Digital evidence amplifies errors when not properly analysed.

Taxpayer Rights in Relation to Digital Evidence

Taxpayers have the right to:

Inspect electronic material relied upon

Seek copies of digital evidence

Challenge authenticity and relevance

Cross-verify system-generated data

Rebut digital conclusions with explanations and documents

Technology cannot override constitutional fairness.

Best Practices for Taxpayers and Professionals

To manage digital evidence effectively:

Maintain clean digital records

Ensure consistency across systems

Document explanations contemporaneously

Avoid informal business communication channels

Respond precisely to digital allegations

In a digital tax system, your data speaks before you do.

Conclusion

Under the New Income-tax Act, electronic records and digital evidence have transformed tax enforcement.

They enhance transparency and efficiency, but also demand:

Higher compliance discipline

Better documentation

Stronger legal understanding

Digital evidence is powerful, but only lawful, contextual, and corroborated data survives judicial scrutiny.

Technology strengthens the law.

It does not replace it.

Written by:

Abhishek Gupta

Chartered Accountant

Office No. 19, Sagar Building, 4th Floor, Plot-327,

Narshi Natha Street, Masjid Bunder (West),

Mumbai – 400009

📞9324776120

🌐 www.consultguruji.com