Faceless Appeal System: Legal Validity and Procedure

The Faceless Appeal System marks a major transformation in India’s tax dispute resolution framework. Introduced to enhance transparency and eliminate personal interface, the system fundamentally changes how appeals before the first appellate authority are conducted.

Under the Income-tax Act, 2025, faceless appeals are no longer transitional. They are an integral part of the appellate mechanism, subject to legal safeguards and judicial scrutiny.

Concept of Faceless Appeal

The faceless appeal system replaces traditional physical hearings with a technology-driven process where:

Appeals are allocated electronically

Communication takes place exclusively through the income-tax portal

Appellate officers remain anonymous

Hearings, where granted, are conducted via video conferencing

The objective is to ensure neutral, unbiased, and standardised appellate decisions.

Legal Validity of the Faceless Appeal System

The faceless appeal framework derives its authority directly from the Income-tax Act and the rules notified thereunder.

Courts have upheld its validity on the condition that:

Principles of natural justice are followed

Adequate opportunity of hearing is granted

Orders are reasoned and speaking

Procedural fairness is not compromised by automation

Faceless does not mean discretion-less. It means process-driven adjudication.

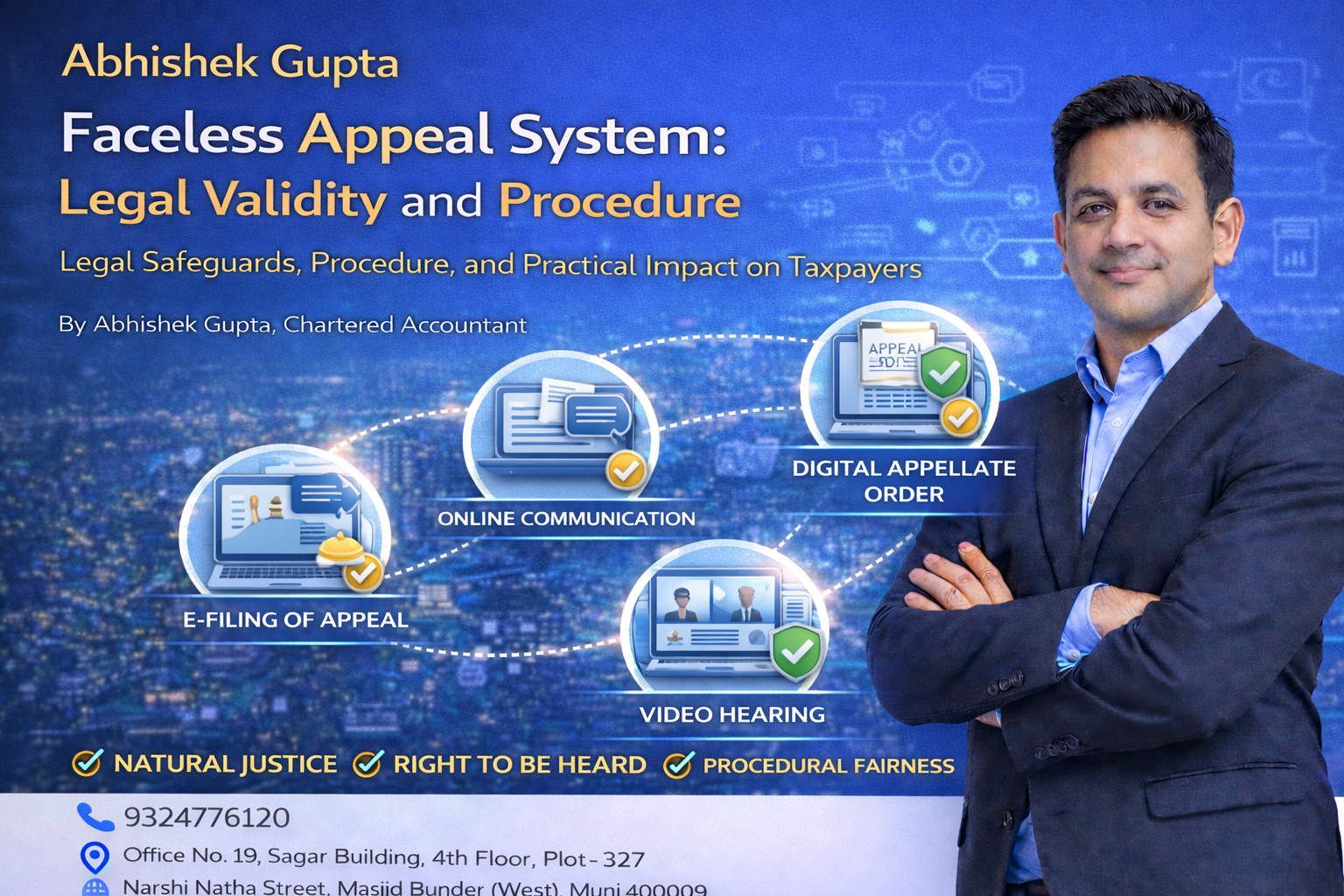

Procedure under the Faceless Appeal System

The appellate process broadly involves:

Electronic filing of appeal

Submission of written grounds and statements

Upload of documentary evidence

Exchange of notices and replies online

Optional video conference hearing

Passing of digital appellate order

Each stage is time-bound and system-tracked.

Right to Personal Hearing

A key safeguard under the faceless appeal system is the right to seek a personal hearing through video conferencing.

If complex factual or legal issues are involved, denial of hearing without reasons can invalidate the appellate order.

Judicial forums have consistently held that effective hearing is a substantive right, not a formality.

Challenges in Faceless Appeals

Despite its objectives, faceless appeals face practical challenges:

Mechanical disposal of appeals

Over-reliance on written submissions

Limited appreciation of business realities

Inadequate consideration of evidence

These issues have led to increased scrutiny by higher appellate authorities.

Impact on Tax Litigation

In the long run, faceless appeals are expected to:

Reduce subjectivity in appellate decisions

Improve consistency across jurisdictions

Lower interpersonal disputes

However, improper implementation may result in:

Increased ITAT litigation

Higher writ petitions on natural justice grounds

Quality of adjudication remains the decisive factor.

Taxpayer Responsibilities

Under faceless appeals, taxpayers must:

Draft precise and structured submissions

Upload complete evidence

Monitor portal communications closely

Respond within strict timelines

There is no scope for oral persuasion beyond written clarity.

Conclusion

The Faceless Appeal System is legally valid and constitutionally sound when implemented with fairness and procedural discipline.

It represents a shift from personality-driven justice to process-driven justice.

For taxpayers, success depends on preparation, documentation, and digital vigilance.

Faceless appeal is not weaker appeal.

It is a different appeal, demanding higher precision

Written by:

Abhishek Gupta

Chartered Accountant

Office No. 19, Sagar Building, 4th Floor, Plot-327,

Narshi Natha Street, Masjid Bunder (West),

Mumbai – 400009

📞9324776120

🌐 www.consultguruji.com