Treatment of Pending Assessments Initiated under 1961 Act

With the enactment of the new Income-tax Act, a key transitional issue arises: what happens to assessments that were initiated under the Income-tax Act, 1961 but remain pending?

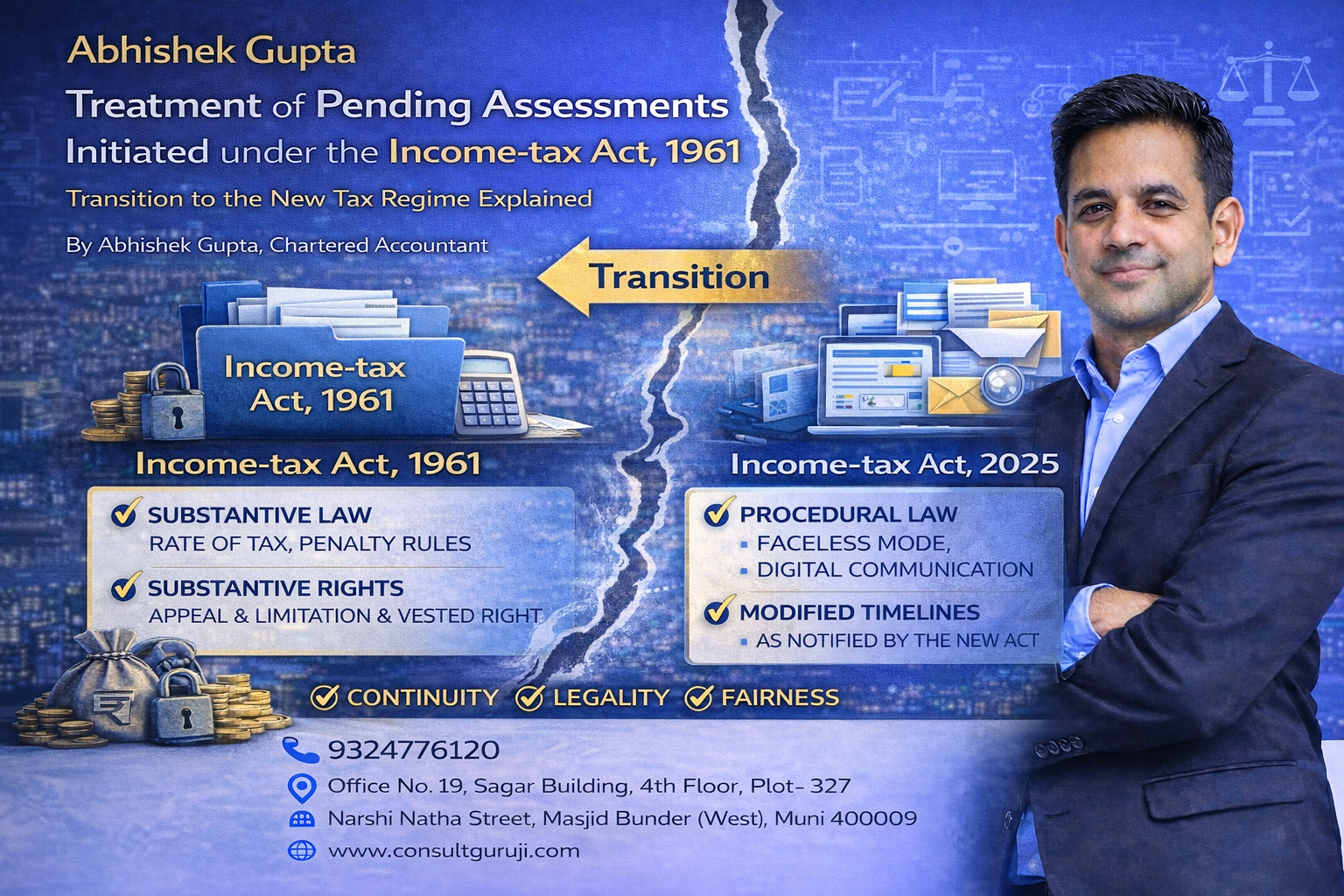

The law does not permit such proceedings to vanish or restart arbitrarily. Instead, it provides a structured mechanism to ensure continuity, legality, and fairness during the transition.

Understanding this treatment is critical for taxpayers facing ongoing scrutiny, reassessment, appeal, or penalty proceedings.

Concept of Pending Assessments

Pending assessments include proceedings that were:

Validly initiated under the Income-tax Act, 1961

Not concluded as on the date the new Act came into force

These may include:

Scrutiny assessments

Reassessments

Rectification proceedings

Penalty proceedings

Recovery proceedings

Appeals at various stages

The key factor is initiation under the old law and continuation into the new regime.

Principle of Continuity

The foundational principle governing transition is continuity of proceedings.

Pending proceedings do not abate merely because the governing statute has changed. Instead:

Proceedings continue from the stage at which they were pending

Rights and obligations already crystallised are preserved

Procedural changes may apply prospectively

This ensures legal certainty and prevents administrative chaos.

Applicable Law for Pending Assessments

In general:

Substantive rights and liabilities are governed by the Income-tax Act, 1961

Procedural aspects may be governed by the new Act, where expressly provided

This distinction is crucial.

Substantive provisions include:

Taxability

Rate of tax

Allowability of deductions

Penalty exposure

Procedural provisions include:

Mode of communication

Faceless mechanisms

Digital processes

Timelines where extended or modified

Courts have consistently upheld this separation between substance and procedure.

Impact on Ongoing Scrutiny and Reassessment

For pending scrutiny or reassessment:

Jurisdiction validly assumed under the 1961 Act remains valid

Notices already issued do not become void

Completion must adhere to principles of natural justice

However, assessments must not:

Apply new substantive provisions retrospectively

Enhance liability beyond what old law permitted

Any such action is legally challengeable.

Effect on Pending Appeals and Litigation

Appeals filed under the 1961 Act:

Continue before the same appellate forum

Are decided based on substantive law applicable to the relevant assessment year

Procedural changes, such as faceless appeal mechanisms, may apply if notified and consistent with natural justice.

Right of appeal is a vested right, and cannot be taken away by transition.

Penalty and Prosecution Proceedings

Penalty proceedings initiated under the 1961 Act:

Continue under the same statutory framework

Must apply penalty provisions as they existed for the relevant year

Similarly, prosecution proceedings are governed by:

Law in force at the time of alleged offence

Not by subsequent amendments unless expressly stated

Taxpayer Safeguards during Transition

Taxpayers retain the right to:

Challenge jurisdictional defects

Object to retrospective application of law

Seek benefit of favourable judicial interpretations

Invoke principles of natural justice

Transition cannot be used as a tool to worsen taxpayer position.

Common Areas of Dispute

Disputes typically arise on:

Application of new limitation periods

Use of faceless procedures in old cases

Change in recovery mechanism

Enhancement of penalty exposure

These issues are expected to be litigated and clarified through judicial precedents.

Conclusion

The treatment of pending assessments initiated under the Income-tax Act, 1961 is governed by continuity, legality, and fairness.

The new Income-tax Act does not erase the past. It carries it forward with structure.

For taxpayers, the key is vigilance:

Understand which law applies

Separate substance from procedure

Assert rights where transition is misapplied

A lawful transition preserves confidence in the tax system.

Anything else invites litigation.

Written by:

Abhishek Gupta

Chartered Accountant

Office No. 19, Sagar Building, 4th Floor, Plot-327,

Narshi Natha Street, Masjid Bunder (West),

Mumbai – 400009

📞9324776120

🌐 www.consultguruji.com