Assessment Procedure under Income-tax Act, 2025: Section-wise Comparison with Income-tax Act, 1961

Introduction

The Income-tax Act, 2025 introduces a reorganised and simplified assessment framework while retaining the core principles of assessment under the Income-tax Act, 1961. The objective is to improve clarity, reduce litigation, and make assessment procedures easier to understand for taxpayers and professionals.

This article explains how assessment-related provisions have been restructured in the new Act through a section-wise comparison with the old law.

Assessment under the Income-tax Act, 1961

Under the Income-tax Act, 1961, assessment procedures were spread across multiple chapters and sections such as:

Section 143 – Regular assessment

Section 144 – Best judgment assessment

Section 147 to 151 – Reassessment provisions

Section 153 – Time limits for completion of assessment

Over the years, frequent amendments led to complexity, overlapping provisions, and interpretational issues.

Assessment Framework under the Income-tax Act, 2025

The Income-tax Act, 2025 reorganises assessment provisions into a more logical and sequential structure. While the substance of law remains largely unchanged, the new Act:

Groups assessment provisions in a consolidated manner

Uses simpler language

Removes redundant explanations and cross-references

This restructuring improves readability and practical application.

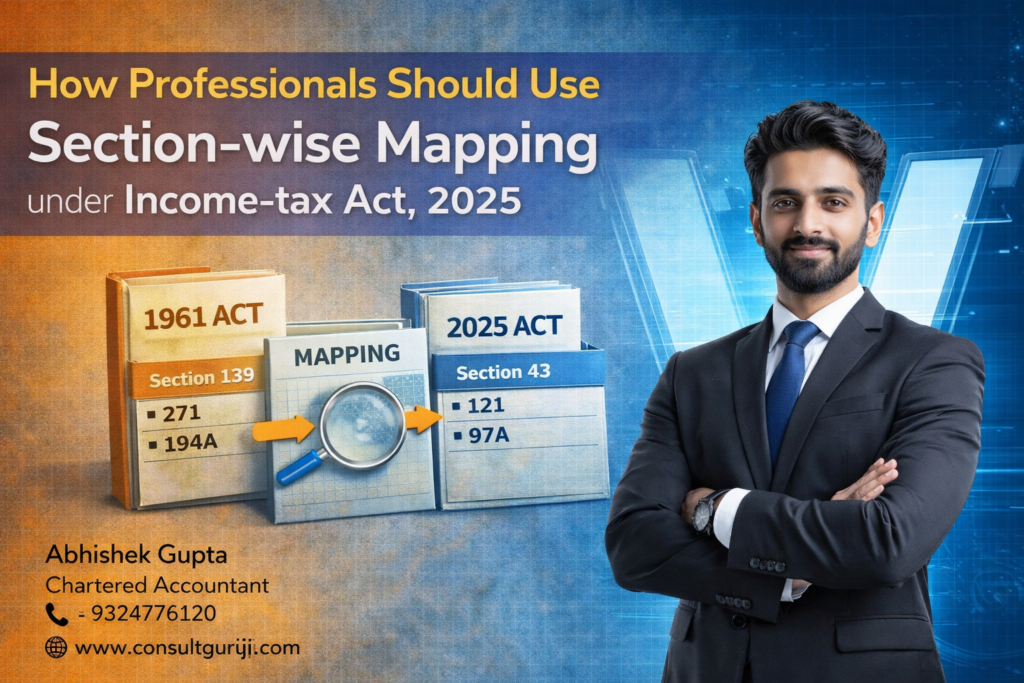

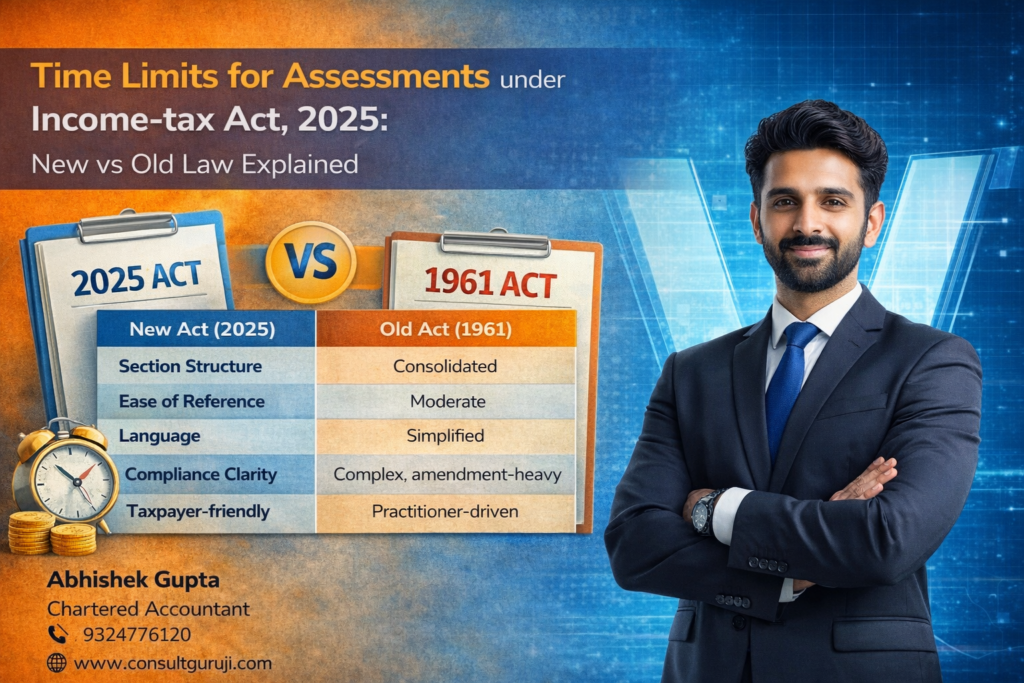

Section-wise Mapping: Old Act vs New Act

Under the new Act, assessment provisions corresponding to Sections 143, 144, 147, and related sections of the 1961 Act are renumbered and placed systematically under a dedicated assessment chapter.

Key improvements include:

Clear distinction between regular assessment, best judgment assessment, and reassessment

Streamlined procedure for issuing notices and passing orders

Better alignment with faceless assessment and digital compliance mechanisms

Time Limits for Assessment

Time-limit provisions, earlier scattered across multiple sections, are now consolidated. This ensures:

Clear understanding of deadlines

Reduced scope for procedural disputes

Faster completion of assessment proceedings

Impact on Taxpayers and Professionals

The reorganised assessment structure under the Income-tax Act, 2025 benefits:

Taxpayers by improving transparency and predictability

Professionals by reducing interpretational ambiguity

Tax administration by enhancing efficiency and consistency

Conclusion

The Income-tax Act, 2025 does not radically change the assessment process but significantly improves its structure and presentation. Taxpayers and professionals should familiarise themselves with the new section numbers and layout to ensure smooth compliance and effective representation.

Written by

Abhishek Gupta

Chartered Accountant

Office No. 19, Sagar Building, 4th Floor, Plot-327,

Narshi Natha Street, Masjid Bunder (West),

Mumbai – 400009

📞 9324776120

🌐 www.consultguruji.com