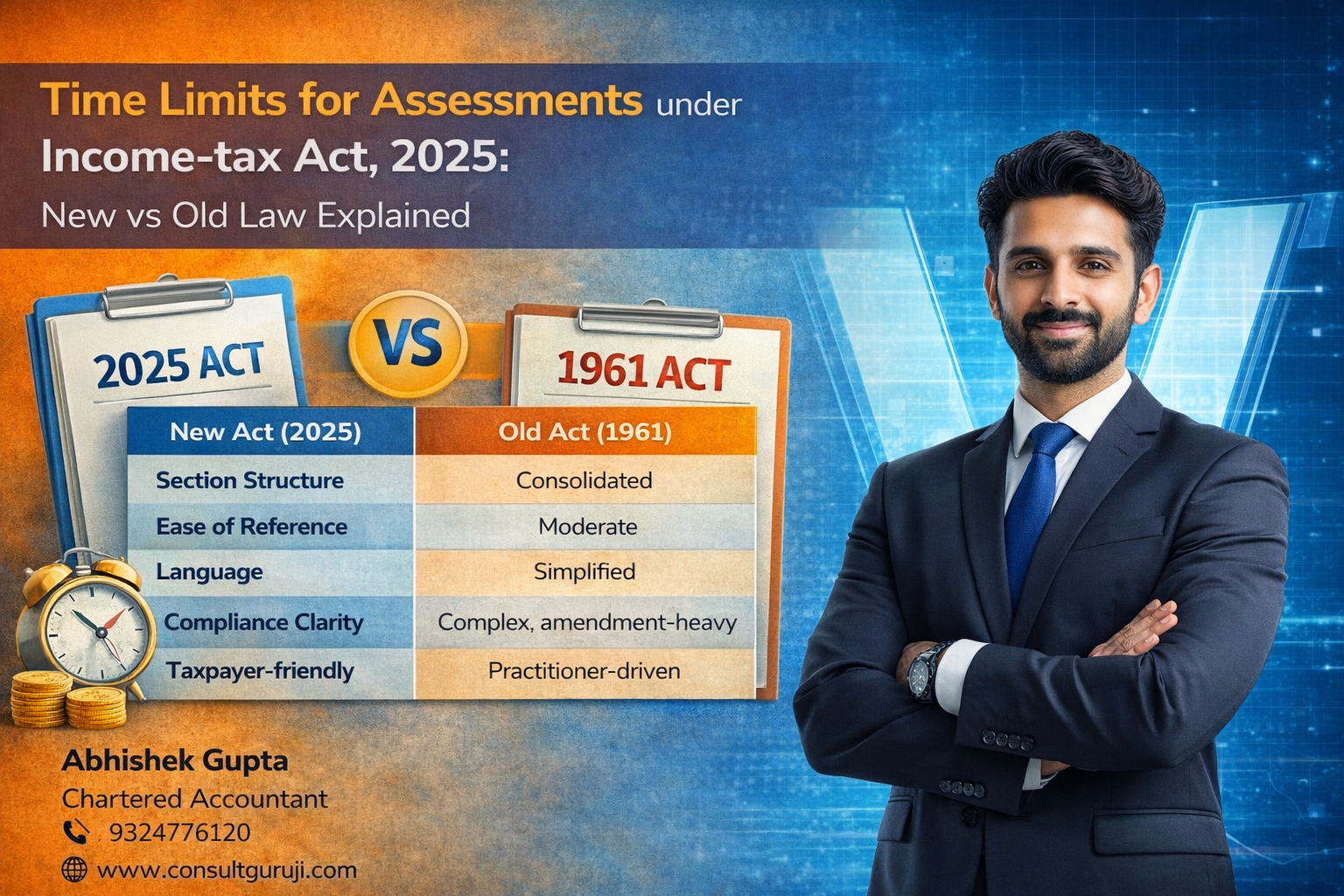

Time Limits for Assessments under Income-tax Act, 2025: New vs Old Law Explained

Introduction

Time limits for completion of assessment are critical for both taxpayers and tax authorities. The Income-tax Act, 2025 has reorganised and rationalised the assessment timelines that earlier existed under the Income-tax Act, 1961. While the core intent remains the same, the new Act brings clarity, consolidation, and easier reference through revised section numbering.

This article explains how assessment time limits under the new Act compare with the old law.

Assessment Time Limits under the Old Law (Income-tax Act, 1961)

Under the 1961 Act, time limits were scattered across multiple sections such as:

Section 143 / 144 – Regular assessment

Section 147 / 148 – Reassessment

Section 153 – Time limit for completion of assessment

Section 153A / 153C – Search and seizure cases

Key challenges:

Multiple amendments over years

Different timelines for different proceedings

Complex cross-referencing between sections

Assessment Time Limits under the New Law (Income-tax Act, 2025)

The 2025 Act restructures these provisions by:

Grouping all assessment timelines in a logical sequence

Clearly distinguishing between:

Regular assessment

Reassessment

Search-related assessment

Removing redundant provisos and explanations

The new structure makes it easier to identify:

Starting point of limitation

Maximum time available to the Assessing Officer

Special cases where extended timelines apply

Key Differences: Old vs New Law

Particulars Old Act (1961) New Act (2025)

Section structure Scattered Consolidated

Ease of reference Moderate High

Language Complex, amendment-heavy Simplified

Compliance clarity Practitioner-driven Taxpayer-friendly

What This Means for Taxpayers

Better predictability in assessment closure

Reduced litigation on limitation issues

Easier tracking of assessment deadlines

Improved transparency in tax administration

Conclusion

The Income-tax Act, 2025 does not drastically change assessment timelines but significantly improves their presentation and accessibility. By reorganising the law, it reduces ambiguity and enhances compliance efficiency for both taxpayers and professionals.

Understanding these timelines is essential to safeguard your rights and ensure timely responses during assessment proceedings.

Written by:

Abhishek Gupta

Chartered Accountant

Office No. 19, Sagar Building, 4th Floor, Plot-327,

Narshi Natha Street, Masjid Bunder (West),

Mumbai – 400009

📞 9324776120

🌐 www.consultguruji.com